HMO Property: The Ultimate Guide (2026)

HMO property is one of the most popular — and most regulated — investment strategies in UK residential property. Whether you're a first-time landlord considering your first house in multiple occupation or an experienced investor looking to scale a portfolio, this guide covers everything you need to know in 2026.

We'll walk through what an HMO actually is, the different types, licensing and planning requirements, fire safety and compliance obligations, how to finance and insure an HMO, the tax implications, and how to find tenants and manage the property day to day.

This is a long read. Use the contents below to jump to the section that matters most to you.

What Is an HMO Property?

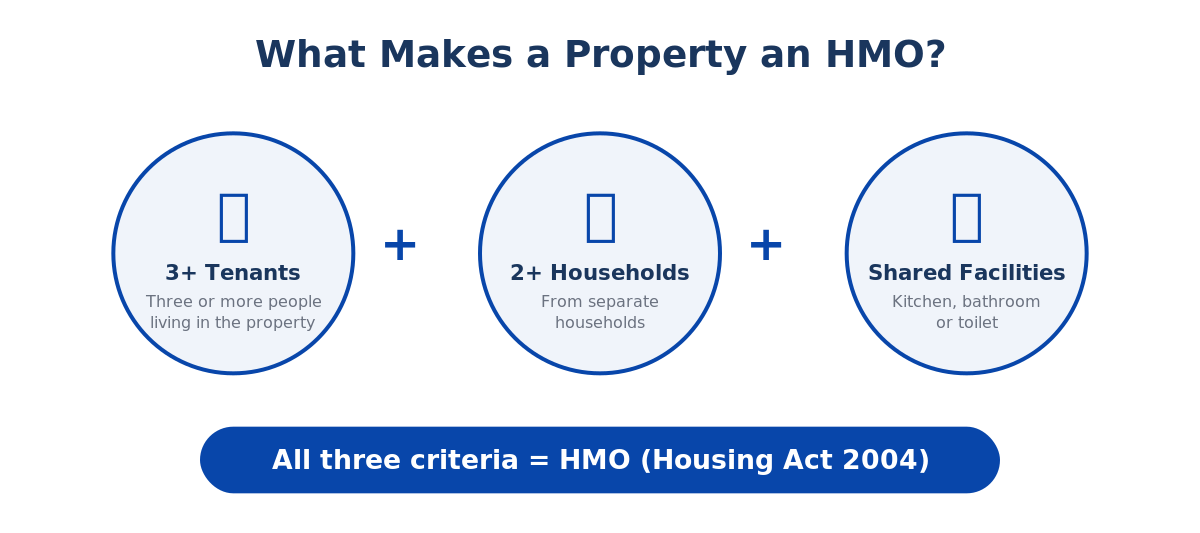

An HMO — or House in Multiple Occupation — is a residential property rented out to three or more tenants who form two or more separate households and share facilities such as a kitchen, bathroom or toilet.

The term comes from the Housing Act 2004, which provides the legal framework for how HMOs are defined, licensed and regulated in England and Wales. Scotland and Northern Ireland have their own, broadly similar legislation.

The Legal Definition (Housing Act 2004)

Under Section 254 of the Housing Act 2004, a property is an HMO if it meets the "standard test":

- It consists of one or more units of living accommodation not consisting of a self-contained flat or flats.

- The living accommodation is occupied by persons who do not form a single household.

- The living accommodation is occupied as the tenants' only or main residence.

- Rents are payable or other consideration is provided.

- Two or more of the households share one or more basic amenities (toilet, bathroom, kitchen) or the accommodation lacks one or more of these.

In practice, the most common example is a house where individual rooms are let to separate tenants who share a communal kitchen and bathroom. But the definition is wider than many landlords realise.

What Counts as a "Household"?

A household is generally a single person, a couple, or members of the same family living together. Two friends renting a property together form two separate households, even if they are on a joint tenancy. A couple sharing a room is one household.

This distinction matters because the number of households — not just the number of tenants — determines whether a property qualifies as an HMO and which licensing requirements apply.

When Does a Property Become an HMO?

A property becomes an HMO as soon as it meets the legal criteria above. There is no formal "registration" that converts it. If you let a four-bedroom house to three unrelated individuals who share a kitchen and bathroom, that property is an HMO by law — regardless of whether you have applied for a licence.

Many landlords inadvertently operate HMOs without realising it, particularly when tenants add partners or friends to the property. Understanding the threshold is essential to avoid enforcement action.

Types of HMO Property

Not all HMOs are the same. The type of HMO you operate affects which licensing regime applies, what planning permission you need, and how lenders will assess a mortgage application.

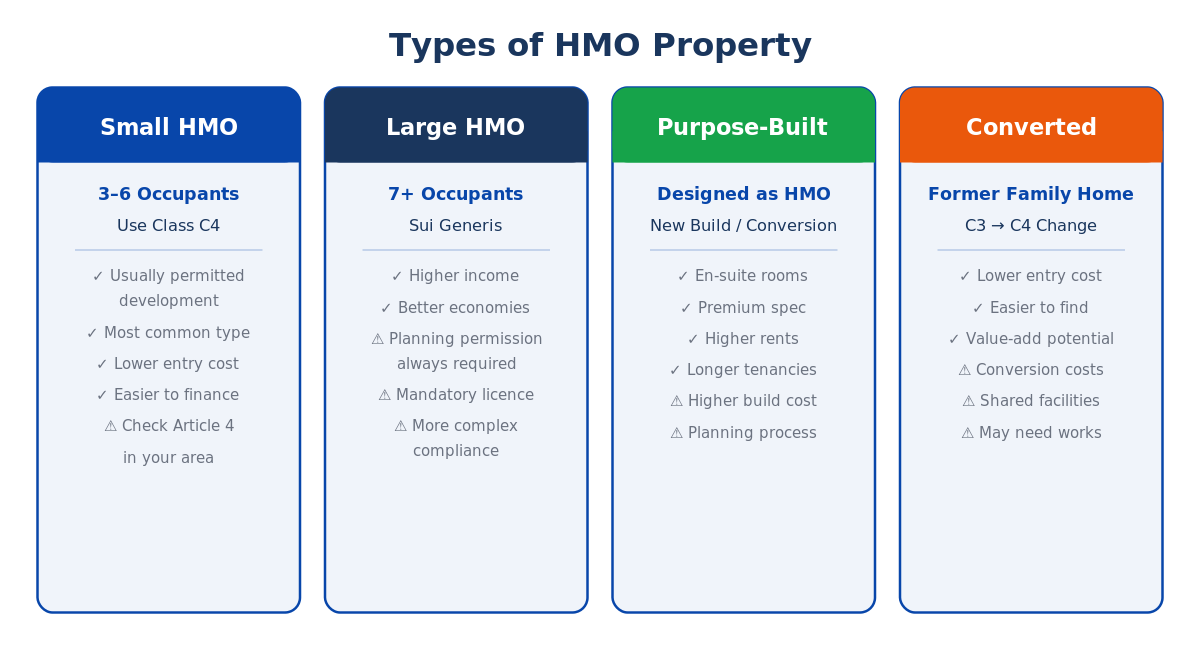

Small HMOs (3–6 Occupants, Use Class C4)

The most common type. A standard residential property (typically a 3–5 bedroom house) let to between three and six unrelated tenants. Under the Town and Country Planning (Use Classes) Order 1987 (as amended), these fall within Use Class C4 — a "house in multiple occupation."

Converting a dwelling house (C3) to a small HMO (C4) is normally permitted development, meaning no planning application is required — unless an Article 4 direction is in place (more on this below).

Large HMOs (7+ Occupants, Sui Generis)

Properties housing seven or more tenants fall outside the standard C4 use class and are classified as Sui Generis (a use "of its own kind"). Large HMOs always require planning permission for change of use. They also always require a mandatory HMO licence.

Large HMOs are typically bigger properties — converted Victorian houses, former care homes, or purpose-built schemes. They tend to generate higher gross income but come with more complex compliance requirements and higher management overhead.

Bedsits & Non-Self-Contained Units

A bedsit is a single room (or small set of rooms) that serves as a tenant's main living and sleeping space, with shared facilities elsewhere in the building. Bedsit-style HMOs were once the most common form of HMO in the UK and are still prevalent in many cities.

Properties with non-self-contained units — where tenants have their own rooms but share a kitchen, bathroom or both — also fall within the HMO definition.

Converted Flats & Mixed-Use Buildings

A building that has been converted into self-contained flats can still be an HMO under certain conditions. If the conversion did not comply with the Building Regulations 1991 (or later) and fewer than two-thirds of the flats are owner-occupied, the whole building may be treated as an HMO under Section 257 of the Housing Act 2004.

Mixed-use buildings with residential and commercial elements can also contain HMOs if the residential units meet the standard test.

Purpose-Built HMOs

These are properties designed from the outset to be HMOs, often with en-suite bedrooms, communal kitchens and living spaces, and built to current fire safety and space standards. Purpose-built HMOs are increasingly popular with professional developers targeting the young professional market.

They tend to command premium rents and attract longer tenancies, but the build cost and planning process can be more involved.

HMOs vs Co-Living Spaces

The line between HMOs and co-living developments has blurred in recent years. Co-living schemes often market themselves as lifestyle products with hotel-style amenities, concierge services and community events. However, in planning and regulatory terms, most co-living developments are classified as Sui Generis HMOs (or sometimes C3 dwellings) and must comply with the same licensing, fire safety and room size regulations.

The key difference is commercial rather than legal: find out more typically targets a younger, higher-income demographic and charges significantly higher rents per room.

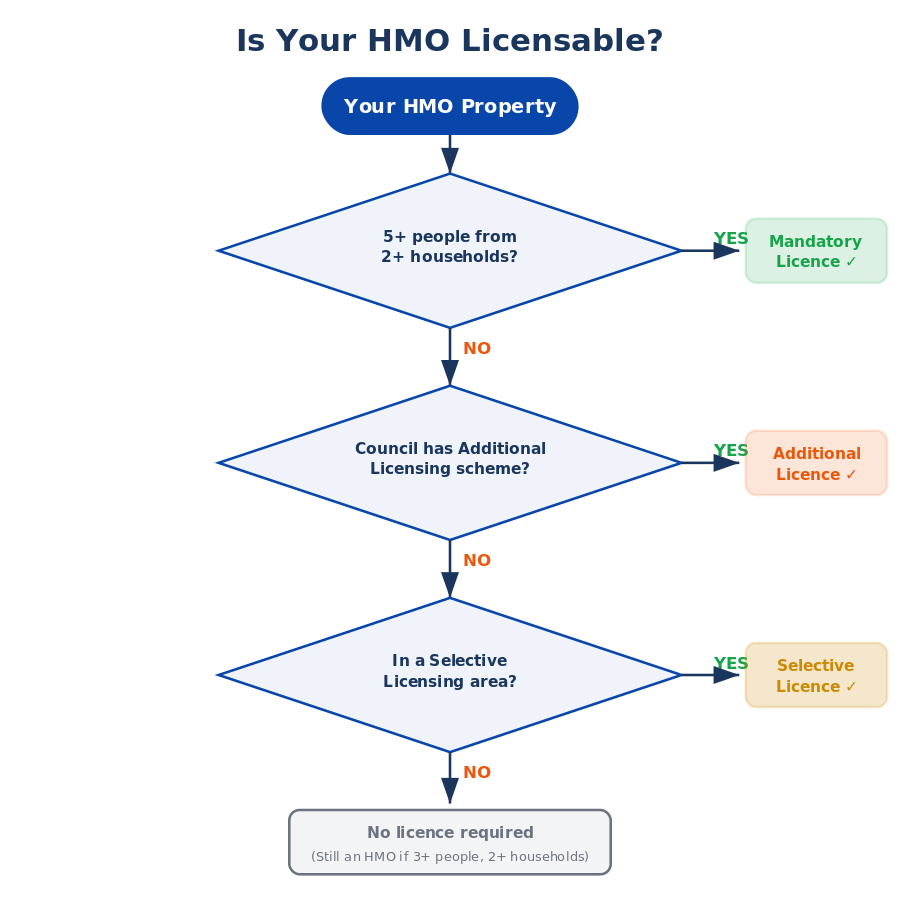

HMO Licensing Explained

HMO licensing decision tree: mandatory licensing for 5+ people from 2+ households, additional licensing schemes, and selective licensing areas">

HMO licensing decision tree: mandatory licensing for 5+ people from 2+ households, additional licensing schemes, and selective licensing areas">

Licensing is arguably the single most important regulatory requirement for any HMO landlord. Operating without the correct licence can result in unlimited fines and rent repayment orders covering up to 12 months of rent.

For a full breakdown, read our complete HMO licensing guide. Below is a summary of the three licensing regimes.

Mandatory Licensing (5+ Tenants, 2+ Households)

Since October 2018, mandatory HMO licensing applies to any property occupied by five or more people forming two or more separate households, regardless of the number of storeys. Before 2018, the mandatory scheme only applied to properties of three or more storeys, but this restriction was removed by the Licensing of Houses in Multiple Occupation (Prescribed Description) (England) Order 2018.

Every local authority in England must operate the mandatory licensing scheme. If your property meets the threshold, you must apply for a licence — there is no opt-out.

Additional Licensing Schemes

Local councils have the power to introduce additional licensing schemes under Section 56 of the Housing Act 2004. These schemes extend licensing requirements to HMOs that fall below the mandatory threshold — typically properties with three or four tenants forming two or more households.

Additional licensing schemes vary by council and must be formally designated. Check with your local authority to see whether one applies in your area.

Selective Licensing Schemes

Selective licensing (Section 80, Housing Act 2004) goes further still, requiring a licence for all privately rented properties in a designated area — not just HMOs. Selective licensing is typically introduced in areas with low housing demand, anti-social behaviour or poor property conditions.

If your HMO is in a selective licensing area, you may need both an HMO licence and a selective licence depending on the council's scheme.

How to Apply for an HMO Licence

The application process is broadly similar across councils, though forms, fees and processing times vary. You will typically need to submit:

- A completed application form (usually online)

- Proof of ownership or management of the property

- Floor plans showing room dimensions

- Gas safety certificate (current)

- Electrical installation condition report (EICR)

- Fire risk assessment

- Energy performance certificate (EPC)

- Details of the proposed licence holder and manager

- The application fee

Councils will inspect the property and may attach conditions to the licence, such as maximum occupancy numbers, required safety works, or restrictions on room usage.

HMO Licence Costs by Council

Licence fees vary significantly. As of 2026, most councils charge between £500 and £1,500 for a five-year mandatory HMO licence, though some London boroughs and major cities charge upwards of £1,000–£1,800. Some councils offer discounts for early applications, accredited landlords, or online submissions.

Fees are generally split into two parts: a first payment on application and a second payment on grant. Factor these costs into your investment analysis — they are an unavoidable operating expense.

Licence Renewal & Expiry

HMO licences are typically granted for five years. You must apply for renewal before the existing licence expires. Operating with an expired licence carries the same penalties as operating without one.

Many councils send reminders, but the legal responsibility lies with the licence holder. Set a calendar reminder at least three months before expiry.

Penalties for Operating Without a Licence

The penalties for operating an unlicensable HMO without a licence are severe:

- Unlimited fines — there is no cap on the fine a court can impose

- Civil penalty notices — councils can issue financial penalties of up to £30,000 per offence as an alternative to prosecution

- Rent repayment orders — tenants (or the local authority) can apply to a First-tier Tribunal to recover up to 12 months' rent

- Banning orders — persistent offenders can be banned from letting or managing properties altogether

These penalties apply even if the property is well maintained and the landlord was genuinely unaware of the licensing requirement. Ignorance is not a defence.

Planning Permission for HMOs

Planning permission is a separate requirement from licensing. While licensing deals with the ongoing management and safety of the property, planning permission deals with the use of the building.

For the full picture, read our HMO planning permission guide.

When Is Planning Permission Required?

Whether you need planning permission to operate an HMO depends on the size of the HMO and whether your local authority has imposed an Article 4 direction:

- Small HMOs (C4, up to 6 occupants): Normally permitted development from C3 (dwelling house) to C4. No planning application needed — unless an Article 4 direction applies.

- Large HMOs (Sui Generis, 7+ occupants): Always require planning permission. The change from C3 or C4 to Sui Generis is not permitted development.

C3 vs C4 vs Sui Generis Use Classes

Understanding use classes is essential for HMO investors:

| Use Class | Description | Example |

|---|---|---|

| C3 | Dwelling house | Family home or up to 6 people living as a single household |

| C4 | House in multiple occupation | 3–6 unrelated tenants sharing facilities |

| Sui Generis | Use of its own kind | 7+ tenants, or other uses outside defined classes |

The distinction matters for both planning applications and property valuations. Sui Generis properties may be valued differently and can be harder to sell to owner-occupiers.

Article 4 Directions Explained

An Article 4 direction is a planning tool that allows a local authority to remove permitted development rights in a specified area. Where an Article 4 direction applies, converting a C3 dwelling to a C4 HMO requires a full planning application — even for small HMOs.

Article 4 directions are increasingly common in university towns and cities with high concentrations of HMOs. They are designed to give councils greater control over the mix of housing types in an area.

For more detail on Article 4 areas, see our Article 4 directions guide.

How to Check If Your Area Has Article 4

Check your local authority's planning pages. Most councils publish a map or list of streets/wards covered by Article 4 directions. You can also call the planning department directly.

Before purchasing any property intended for HMO use, always confirm the planning position. Buying a property in an Article 4 area without checking could leave you unable to operate it as an HMO.

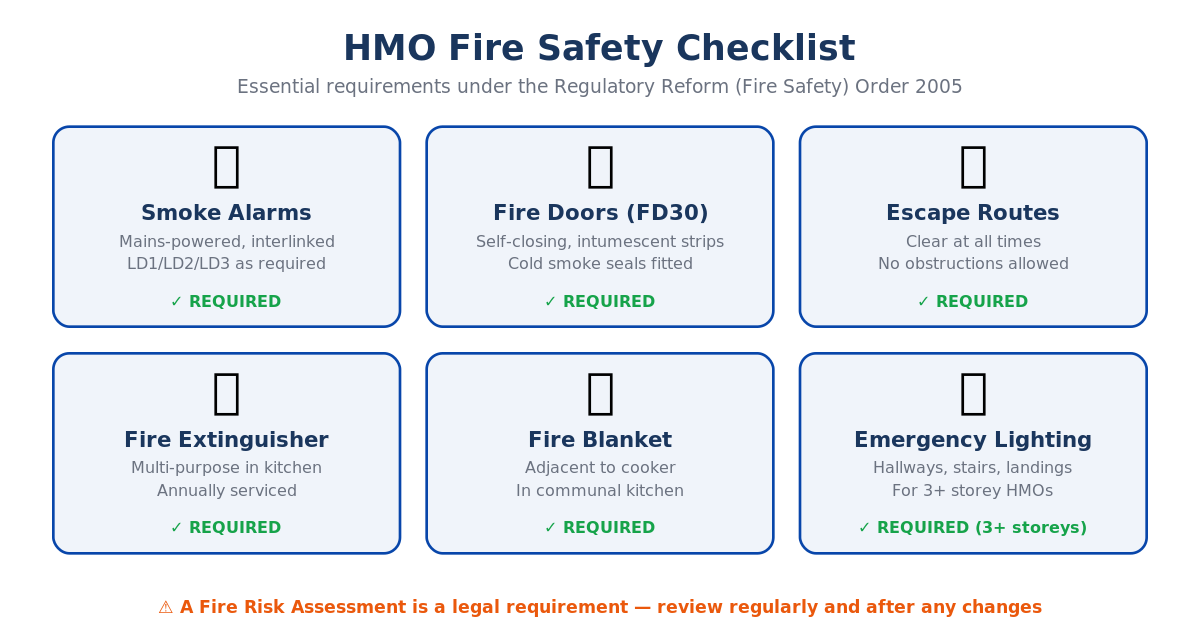

HMO Fire Safety Requirements

Fire safety is the area of HMO compliance where cutting corners can have fatal consequences. HMOs are inherently higher risk than single-occupancy dwellings because multiple unrelated occupants may be less familiar with the property layout and escape routes.

Fire Doors (FD30 Standard)

All HMOs with three or more storeys (and many smaller HMOs depending on local council requirements) must have FD30-rated fire doors on every habitable room opening onto a communal hallway or staircase. FD30 doors are certified to resist fire for 30 minutes.

Fire doors must be fitted with:

– Self-closing devices (overhead closers or rising butt hinges)

– Intumescent strips and cold smoke seals

– Correct door furniture (no letter plates on fire doors to escape routes)

Smoke & Fire Alarm Systems (LD1, LD2, LD3)

HMOs require an appropriate fire detection system. The required grade depends on the size and layout:

- LD3 (Grade D): Minimum standard — mains-powered smoke alarms on escape routes and in communal areas. Suitable for some smaller HMOs.

- LD2 (Grade A): Mains-powered, interlinked fire detection in escape routes, communal areas and high-risk rooms (kitchens, living rooms). Required for most HMOs with three or more storeys.

- LD1 (Grade A): Full coverage in every habitable room and escape route. Required for large HMOs and where councils specify it as a licence condition.

Your local council's licensing conditions will specify the minimum detection grade. Always check before assuming LD3 is sufficient.

Fire Extinguishers & Fire Blankets

Most councils require fire extinguishers and fire blankets in communal kitchens. The specific requirements vary, but a minimum of one fire blanket adjacent to the cooker and one multi-purpose fire extinguisher in the kitchen is typical.

Escape Routes & Emergency Lighting

All escape routes must be kept clear at all times. In HMOs of three or more storeys, emergency lighting is normally required in communal hallways, staircases and landings to ensure safe evacuation in the event of a power failure.

Escape windows may be required in rooms where the only exit route passes through a high-risk area (such as a kitchen).

Fire Risk Assessments

Under the Regulatory Reform (Fire Safety) Order 2005, the "responsible person" (usually the landlord or managing agent) must carry out a fire risk assessment and keep it under regular review. This is a legal requirement, not a recommendation.

A fire risk assessment should identify hazards, evaluate the risk to occupants, and set out measures to reduce or eliminate those risks. Many landlords commission a professional fire risk assessor, particularly for larger HMOs.

The Fire Safety (England) Regulations 2022

The Fire Safety (England) Regulations 2022, which came into force on 23 January 2023, placed additional duties on responsible persons for buildings containing two or more sets of domestic premises. For HMO landlords, this includes requirements to share fire door information with residents, provide fire safety instructions, and in some cases carry out regular fire door inspections.

Minimum Room Sizes for HMOs

Room sizes in HMOs are strictly regulated. These are legal minimums, not recommendations — licensing a room below these thresholds is a criminal offence.

Bedroom Size Requirements

The Licensing of Houses in Multiple Occupation (Mandatory Conditions of Licences) (England) Regulations 2018 set the following national minimum sleeping room sizes:

| Room type | Minimum floor area |

|---|---|

| Single bedroom (1 person aged 10+) | 6.51 m² |

| Double bedroom (2 persons aged 10+) | 10.22 m² |

| Child under 10 | 4.64 m² |

These are absolute minimums. Many councils impose larger minimum sizes through their licensing conditions — particularly for rooms that also contain cooking facilities.

Any room below 4.64 m² cannot be used as sleeping accommodation at all.

Kitchen & Bathroom Facility Ratios

Councils set their own standards for kitchen and bathroom provision, but typical ratios include:

- Bathroom/WC: One bathroom with a bath or shower, one separate WC (or combined bathroom/WC) per 5 occupants

- Kitchen: Cooking facilities for every 5 occupants, with adequate worktop space, food storage, and refrigeration

- Wash hand basin: One in each WC (or bathroom if combined)

Some councils require en-suite facilities for rooms above a certain occupancy level or in properties above a certain total size.

Ceiling Height Rules

Rooms with sloping ceilings (such as attic conversions) present a particular issue. Any floor area where the ceiling height is below 1.5 metres cannot be counted towards the discover more. This means an attic room may look spacious but fail to meet the legal minimum once the angled ceiling areas are excluded.

How Room Sizes Affect Licence Conditions

Your HMO licence will specify the maximum number of occupants permitted in each room based on its measured floor area. Exceeding these numbers is a licence condition breach and can result in enforcement action.

If you are planning an HMO conversion, measure every room carefully and cross-check against both the national minimums and your local council's specific standards before committing to a layout.

HMO Health & Safety Compliance

Beyond fire safety and room sizes, HMO landlords must meet a range of health and safety obligations. For a practical checklist, see our HMO compliance checklist.

Gas Safety Certificates (Annual)

If your HMO has a gas supply, you must have all gas appliances, fittings and flues inspected by a Gas Safe registered engineer every 12 months. A copy of the gas safety certificate must be provided to existing tenants within 28 days of the check and to new tenants before they move in.

This is a requirement under the Gas Safety (Installation and Use) Regulations 1998.

Electrical Safety (EICR Every 5 Years)

The Electrical Safety Standards in the Private Rented Sector (England) Regulations 2020 require landlords to have the electrical installation inspected and tested by a qualified person at least every 5 years. The resulting Electrical Installation Condition Report (EICR) must show the installation as satisfactory.

If the EICR identifies any unsatisfactory findings (coded C1, C2 or FI), the landlord must complete the necessary remedial works within 28 days (or sooner if the issue presents an immediate danger).

Energy Performance Certificates (EPC)

All privately rented properties — including HMOs — must have a valid EPC with a minimum rating of E. Properties rated F or G cannot be legally let unless a valid exemption has been registered on the PRS Exemptions Register.

There are proposals to raise the minimum EPC requirement to C in future, though the timeline has been subject to delays. Check gov.uk for the latest position.

HHSRS Risk Assessments

The Housing Health and Safety Rating System (HHSRS) is the methodology used by local authorities to assess health and safety hazards in residential properties. It covers 29 hazard categories including excess cold, falls, fire, damp and mould, noise, and overcrowding.

If a council identifies a Category 1 hazard (the most serious), it has a duty to take enforcement action. Category 2 hazards give the council discretionary power to act.

Carbon Monoxide Alarms

The Smoke and Carbon Monoxide Alarm (Amendment) Regulations 2022 require landlords to install a carbon monoxide alarm in any room containing a fixed combustion appliance (excluding gas cookers). This includes rooms with gas boilers, gas fires, or wood-burning stoves.

Alarms must be tested at the start of each new tenancy.

Damp & Mould Obligations (Awaab's Law)

Following the tragic death of Awaab Ishak in 2020 from exposure to mould in social housing, the government introduced Awaab's Law as part of the Social Housing (Regulation) Act 2023. While initially targeted at social housing, the principles are being extended to the private rented sector.

HMO landlords have a duty to investigate reports of damp and mould within 14 days, begin remedial work within 7 days of investigation, and complete emergency repairs within 24 hours where there is an immediate risk to health. These timescales apply to hazards that pose a risk to the health of tenants.

Proactive management of ventilation, heating and damp is essential — both for tenant welfare and to avoid enforcement action.

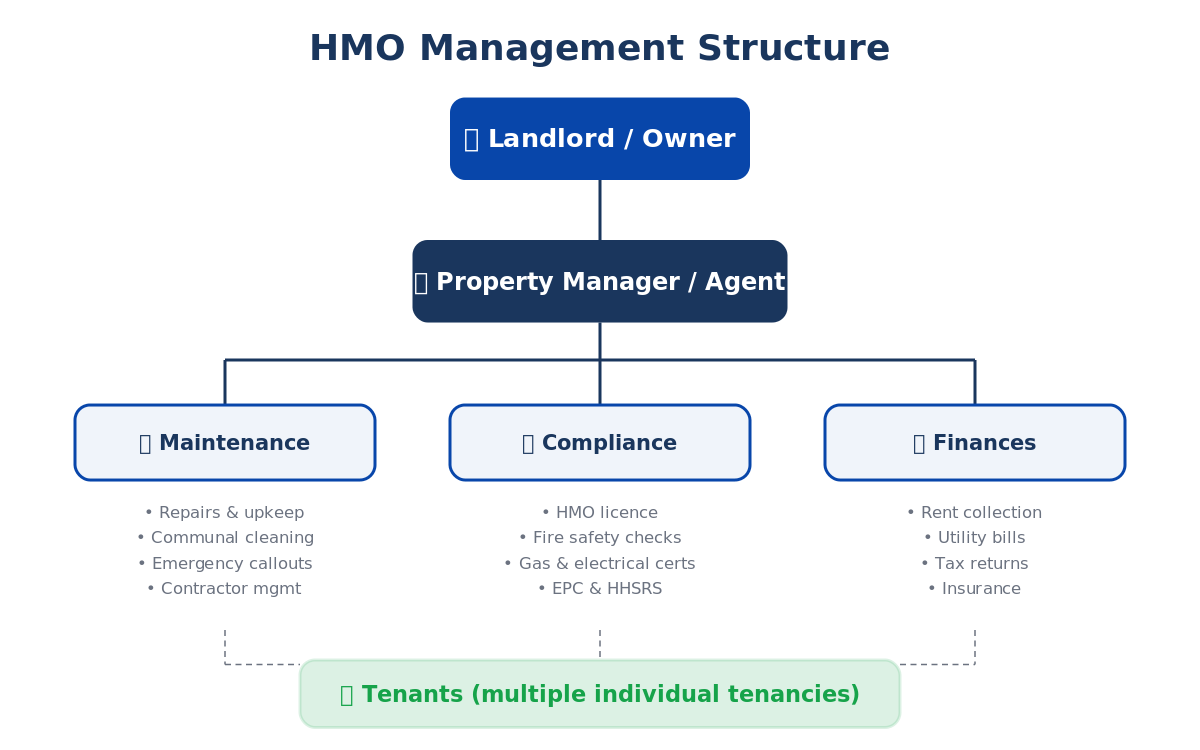

HMO Management Regulations

HMO management structure diagram showing hierarchy from landlord to property manager, with three branches: maintenance, compliance, and finances, all serving tenants">

HMO management structure diagram showing hierarchy from landlord to property manager, with three branches: maintenance, compliance, and finances, all serving tenants">

Running an HMO involves ongoing management responsibilities that go well beyond simply collecting rent. The legal framework is set out in the Management of Houses in Multiple Occupation (England) Regulations 2006 (as amended).

The Management of HMOs (England) Regulations 2006

These regulations impose specific duties on the "manager" of an HMO (usually the landlord or their appointed agent). Key duties include:

- Providing and displaying the manager's name, address and contact details

- Maintaining the structure and exterior of the property

- Keeping all common parts, fixtures and fittings in good repair and clean condition

- Maintaining water supply, drainage and sanitary conveniences

- Maintaining gas and electrical installations in safe working order

- Maintaining fire safety equipment and keeping escape routes clear

- Providing adequate waste disposal facilities

Failure to comply is a criminal offence punishable by an unlimited fine.

Communal Area Maintenance

Communal areas — hallways, staircases, landings, kitchens, bathrooms and any shared living spaces — are the landlord's responsibility. They must be kept clean, in good repair, and free from obstruction.

In practice, many landlords arrange regular professional cleaning (weekly or fortnightly) for communal areas. This is a deductible expense for tax purposes and helps maintain the property's condition and tenant satisfaction.

Waste Disposal & Recycling

The landlord must provide sufficient bins for household waste and recycling and ensure tenants have access to the council's waste collection service. In many HMOs, waste management is an ongoing challenge. Clear house rules, an adequate number of bins, and a rota or communal cleaning schedule can help.

Water Supply & Drainage

The water supply must be maintained in good working order. Storage tanks must be properly covered and insulated. Drainage must be kept unblocked and functional.

Tenant Communication & House Rules

While not a legal requirement, clear house rules covering noise, cleaning rotas, guest policies, waste disposal and use of communal areas are essential for smooth learn more. Most experienced HMO landlords provide a written house handbook to every tenant at move-in.

Self-Management vs Letting Agent vs Rent-to-Rent

How you manage your HMO has a significant impact on your returns and workload:

- Self-management: Maximum control and profit retention. Suitable if you live locally and have the time to handle tenant queries, maintenance issues, viewings and admin. Most profitable per unit but most time-intensive.

- Letting agent: Professional management typically costs 10–15% of gross rent for HMOs (higher than standard BTL rates due to multiple tenancies). A good HMO-specialist agent handles all day-to-day management, but quality varies enormously.

- Rent-to-rent: A third party (the "rent-to-rent operator") takes a lease on your property and manages it as an HMO, paying you an agreed rent. You sacrifice some income for a hands-off arrangement. Risks include the operator going bust or failing to maintain the property to the required standard.

Is HMO Property a Good Investment?

HMO property has been one of the strongest-performing investment strategies in UK residential property for over a decade. But it is not without downsides.

For a detailed analysis, see our HMO property investment guide. Here's the summary.

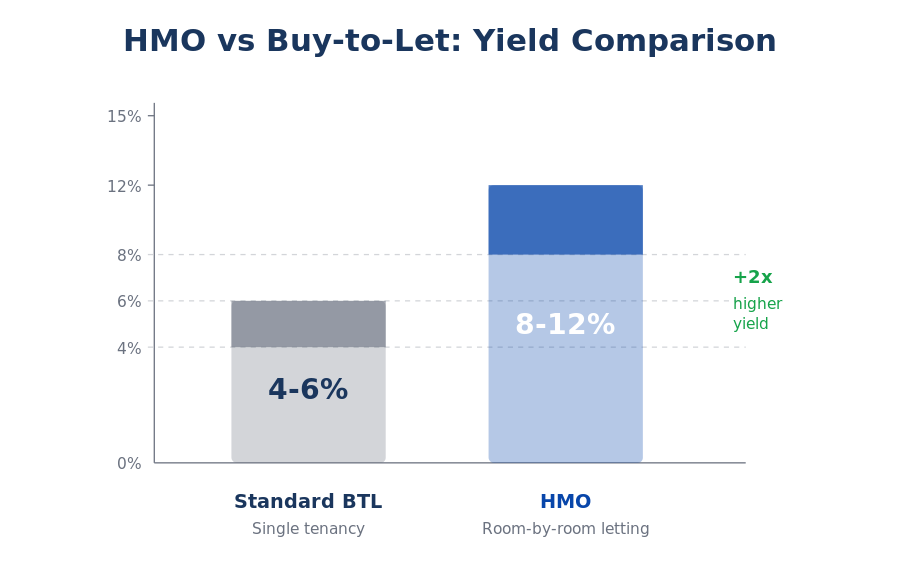

Average HMO Rental Yields vs Buy-to-Let

The core financial advantage of HMOs is simple: renting by the room generates significantly more income than renting a whole property to a single household.

A typical 4-bedroom house in a regional city might generate £800–£1,000/month as a standard buy-to-let. The same property configured as an HMO could generate £1,600–£2,400/month by letting each room individually at £400–£600 per room.

Gross yields on HMOs typically range from 8–15%, compared with 4–7% for standard buy-to-let properties. The premium reflects both the higher income and the additional work and risk involved.

For a direct comparison, see our HMO vs buy-to-let comparison.

Reduced Void Risk (Multiple Income Streams)

With a standard buy-to-let, a single void period means zero income. With a 5-room HMO, losing one tenant reduces income by only 20%. The diversification of income across multiple tenancies significantly reduces void risk.

In practice, well-managed HMOs in strong rental locations can maintain 95%+ occupancy year-round.

Capital Growth Potential

HMOs benefit from the same underlying capital growth as any residential property. Additionally, converting a standard dwelling to an HMO (adding bedrooms, en-suites, upgrading specification) can add value beyond market appreciation alone.

Demand Drivers (Affordability Crisis, Young Professionals, Students)

Demand for HMO rooms continues to grow, driven by:

- Housing affordability: With average house prices exceeding eight times average earnings, many working professionals cannot afford to rent a whole property alone

- Young professional market: Workers aged 22–35 increasingly prefer renting a high-quality room in a shared house to renting a studio or one-bed flat

- Students: The student population continues to grow, underpinning demand in university towns

- Migration and population growth: Net migration and demographic shifts sustain rental demand

For more on managing HMO income, see our guide to HMO income vs expenses.

The Downsides (Higher Management, Regulation, Upfront Costs)

HMOs are not passive investments. The key disadvantages include:

- Higher management burden: More tenants means more queries, more maintenance, more turnover and more admin

- Regulatory complexity: Licensing, fire safety, room sizes, planning — the compliance burden is significantly greater than standard buy-to-let

- Higher upfront costs: Conversion, furnishing, fire safety works and licensing fees can run to £20,000–£50,000+ depending on the property

- Lender restrictions: Not all mortgage lenders will lend on HMOs, and those that do often require higher deposits and charge higher interest rates

- Tenant turnover: HMO rooms typically have shorter average tenancy lengths than whole-property lets, though this varies by market

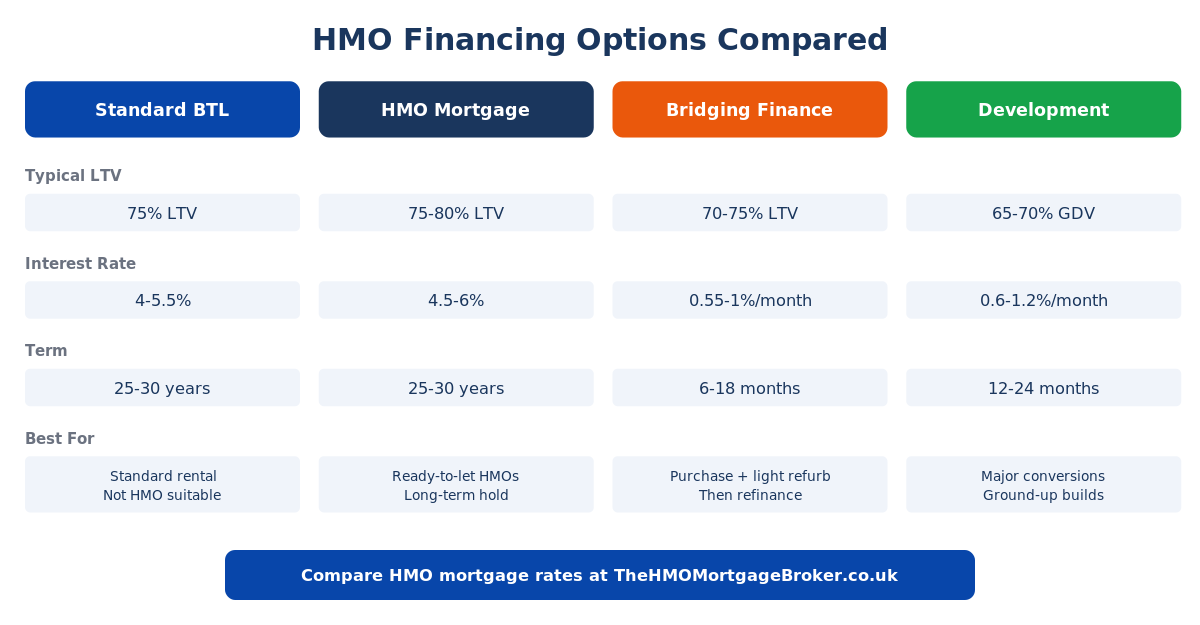

How to Finance an HMO Property

Financing is where many first-time HMO investors get stuck. Standard residential and buy-to-let mortgages are not suitable for HMOs. You need a specialist product.

For live rates and to compare options, visit compare HMO mortgage rates or use our HMO mortgage calculator.

HMO Mortgages Explained

An HMO mortgage is a specialist buy-to-let mortgage designed for properties let as houses in multiple occupation. The key differences from a standard BTL mortgage include:

- Rental assessment: Most HMO lenders assess affordability based on the aggregate room-by-room rental income rather than a single AST market rent

- Property criteria: Lenders specify minimum property values, maximum room numbers, acceptable property types and required safety standards

- Experience requirements: Many lenders require the borrower to have prior landlord experience (often 12+ months owning a rental property)

- Interest rates: HMO mortgage rates are typically 0.25–0.75% higher than standard BTL rates, reflecting the perceived additional risk

Deposit Requirements (Typically 20–25%)

Most HMO mortgage lenders require a minimum deposit of 20–25% of the property value. Some specialist lenders may offer 75–80% LTV products, while a few will go to 80% LTV for borrowers with strong experience and financials.

First-time landlords may face higher deposit requirements. See our guide to HMO mortgage deposits for the full picture.

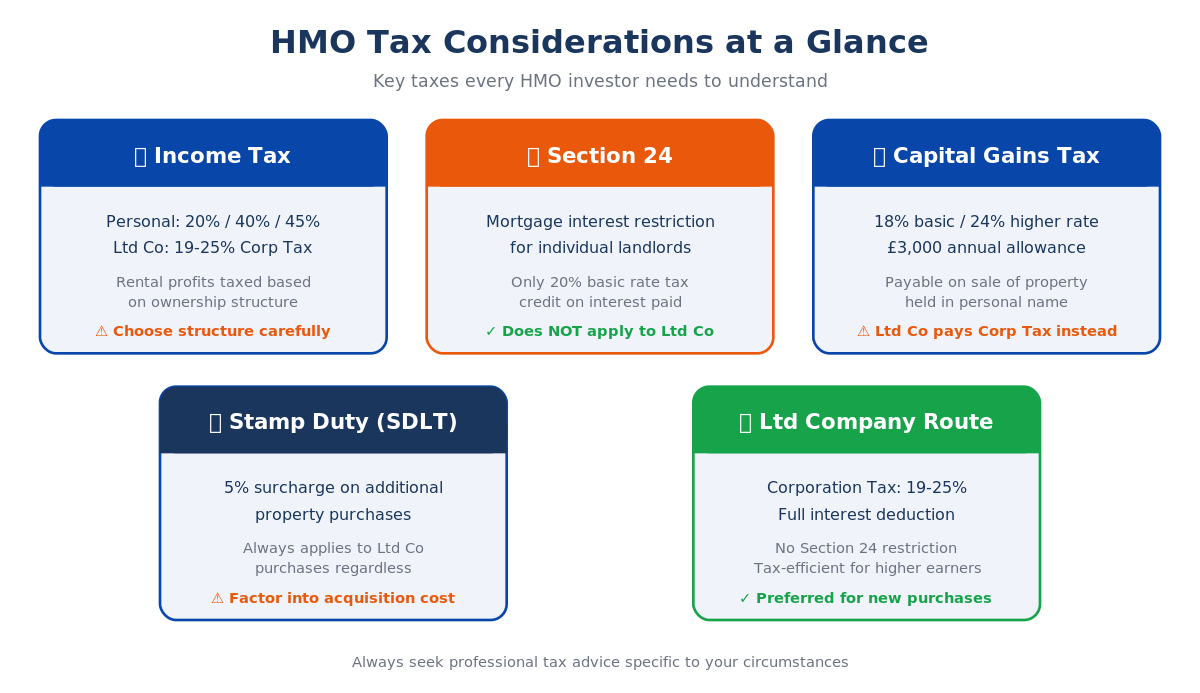

Personal Name vs Limited Company Purchase

One of the most important decisions for any HMO investor is whether to purchase in their personal name or through a limited company (SPV). The implications are primarily tax-related:

- Personal name: Rental income is taxed as income tax (up to 45% for higher/additional rate taxpayers). Section 24 restricts mortgage interest relief to a basic rate tax credit.

- Limited company: Rental profits are subject to corporation tax (currently 25% for profits over £250,000, with marginal relief from £50,000). Full mortgage interest deduction is available as a business expense. Extracting profits requires dividends or salary.

For most higher-rate taxpayers acquiring new HMO properties, a limited company structure is often more tax-efficient. However, the decision involves complex trade-offs including mortgage availability, remortgaging flexibility, and long-term exit strategy. Always take professional tax advice.

Read more on limited company HMO mortgages and the tax implications of limited company HMO mortgages.

Bridging Finance for HMO Conversions

If you are buying a property that needs conversion work before it can be let as an HMO, a standard HMO mortgage may not be available immediately. Bridging finance provides short-term funding (typically 6–18 months) to purchase and refurbish the property, with the plan to refinance onto a long-term HMO mortgage once the works are complete and the property is tenanted.

Bridging rates are higher than term mortgage rates, but the flexibility is invaluable for conversion projects. Learn more in our guide to HMO bridging finance.

Development Finance for Larger Projects

For larger HMO developments — ground-up builds, major conversions, or commercial-to-residential projects — development finance may be more appropriate than bridging. learn more typically funds both the purchase and the build costs, with drawdowns released in stages as works progress.

Remortgaging an HMO

Once your HMO is operational and tenanted, you can typically remortgage onto a better long-term rate. Remortgaging also allows you to release equity for further investment if the property has increased in value (through market growth or the "value add" of the conversion).

For a step-by-step walkthrough, see our guide to remortgaging an HMO.

Ready to compare HMO mortgage options? Compare HMO mortgage rates →

Tax Implications of HMO Property

Tax is one of the most misunderstood aspects of HMO investment. Getting the structure right from the outset can save tens of thousands of pounds over a portfolio's lifetime.

The information below is for general guidance only and does not constitute financial or tax advice. Always consult a qualified accountant or tax adviser for advice specific to your circumstances.

Income Tax vs Corporation Tax

How your HMO income is taxed depends on your ownership structure:

- Personal ownership: Rental profits are added to your other income and taxed at your marginal income tax rate — 20% (basic rate), 40% (higher rate) or 45% (additional rate). National Insurance is not payable on rental income.

- Limited company ownership: Rental profits are subject to corporation tax. From April 2023, the main rate is 25% for companies with profits over £250,000, with a small profits rate of 19% for profits up to £50,000 and marginal relief between the two thresholds.

Section 24 Mortgage Interest Relief Restriction

Since April 2020, individual landlords can no longer deduct mortgage interest payments from rental income before calculating tax. Instead, they receive a basic rate tax credit (20%) on the interest paid.

This means a higher-rate taxpayer paying £10,000/year in mortgage interest on a personally held HMO pays tax on the gross rental income and then receives a £2,000 tax credit — rather than deducting the full £10,000 from taxable income as was previously the case.

Section 24 does not apply to limited companies, which can deduct mortgage interest in full as a business expense. This is one of the primary reasons many HMO investors now purchase through learn more. See the HMRC guidance on restricting finance cost relief for individual landlords.

Allowable Expenses for HMO Landlords

Whether you operate in personal name or through a company, the following expenses are generally deductible against rental income:

- Mortgage interest (company) or eligible for basic rate tax credit (individual)

- Insurance premiums

- Letting agent fees and management costs

- Repairs and maintenance (but not improvements)

- Council tax (if paid by the landlord)

- Utility bills (if included in rent)

- Professional fees (accountant, legal)

- Advertising for tenants

- Cleaning costs for communal areas

- Fire safety equipment and testing

- Gas and electrical safety certificates

- Licence fees

- Furniture and furnishing replacement (under the replacement domestic items relief)

Capital Gains Tax on HMO Sales

When you sell an HMO held in your personal name, any gain is subject to Capital Gains Tax (CGT). The current CGT rates on residential property are 18% (basic rate) and 24% (higher rate), following the changes announced in the Autumn Budget 2024.

Each individual has an annual CGT allowance (£3,000 for 2025/26). Gains above the allowance are taxed at the applicable rate.

For properties held within a limited company, the gain is subject to corporation tax rather than CGT. Extracting the proceeds from the company may then attract additional tax on dividends.

Stamp Duty on HMO Purchases (3% Surcharge)

If you already own a residential property (including your own home) when purchasing an HMO, you will pay the higher rates of Stamp Duty Land Tax (SDLT) — a surcharge of 5% on top of the standard rates (increased from 3% following the October 2024 Budget for completions from 1 April 2025).

For a property purchased for £250,000, the additional SDLT would be £12,500 on top of the standard liability.

Limited company purchases always attract the higher rates, regardless of whether the company already owns property.

VAT Considerations

Residential property rental income is generally exempt from VAT. However, certain services associated with HMOs — such as management services, cleaning services, or furnished holiday lets — may have VAT implications if you are VAT registered or above the VAT threshold (currently £90,000).

HMO Property Insurance

Standard buy-to-let landlord insurance will not cover an HMO. You need a specialist policy.

For a detailed breakdown, read our HMO property insurance guide.

Landlord Buildings & Contents Insurance

HMO buildings insurance covers the physical structure of the property. Contents insurance covers any furnishings, appliances and fixtures you provide as the landlord.

HMO policies are typically more expensive than standard BTL cover because of the higher risk profile — more occupants means more wear and tear, more potential for accidental damage, and greater fire risk.

Public Liability Insurance

Public liability insurance protects you if a tenant, visitor or member of the public is injured on your property due to your negligence. Given the higher footfall in an HMO, this cover is essential. Many HMO insurers include public liability as standard or offer it as an add-on.

Rent Guarantee Insurance

Rent guarantee insurance (RGI) covers lost rental income if a tenant stops paying rent. Given that HMOs have multiple tenancies, some insurers offer room-by-room RGI, though availability and terms vary.

Legal Expenses Cover

Legal expenses insurance covers the cost of pursuing or defending legal action — such as possession proceedings against a non-paying tenant, or defending a claim from a tenant.

Why Standard BTL Insurance Won't Cover an HMO

The key reason is risk. Standard BTL policies are underwritten on the basis of a single tenancy to a family or individual. An HMO with multiple unrelated occupants, higher turnover, shared facilities and different fire safety requirements presents a materially different risk profile. Operating an HMO on a standard BTL policy could void your cover entirely — leaving you exposed in the event of a major claim.

HMO Valuations

Understanding how HMOs are valued is important for purchase, remortgaging and long-term strategy. Read our full guide on how HMO properties are valued.

Bricks & Mortar vs Commercial Valuation

Most residential properties are valued on a bricks and mortar basis — essentially, what a comparable property has sold for recently. This is the standard approach for buy-to-let and smaller HMOs.

Larger HMOs (typically 7+ rooms) and purpose-built HMOs may be valued on a commercial basis, which takes into account the rental income the property generates. A commercial valuation typically uses a capitalisation rate (yield) applied to the net rental income.

How Lenders Value HMOs

Different lenders take different approaches. Some will only use bricks and mortar valuations (treating the HMO as an ordinary house). Others will accept a commercial valuation that reflects the income-generating potential.

This distinction matters because a property generating strong HMO income may be worth significantly more on a commercial valuation than on a bricks and mortar basis — allowing you to release more equity when remortgaging.

How Rental Income Affects Property Value

For properties valued commercially, higher rental income directly translates to a higher valuation. This creates a virtuous cycle: improving room specification, adding en-suites, or achieving above-market rents can increase the property's capital value as well as its cash flow.

Finding & Filling an HMO with Tenants

Having a compliant, well-financed HMO is only half the job. You need tenants.

Best Platforms for HMO Tenant Finding

The most effective channels for finding HMO tenants include:

- SpareRoom — The UK's largest flatshare website and the go-to platform for HMO room lets

- Rightmove and Zoopla — Some agents list HMO rooms, though these platforms are more geared to whole-property lets

- OpenRent — Direct landlord listing platform with room listing options

- Facebook Marketplace and local groups — Effective in many areas, particularly for younger tenants

- University accommodation offices — For student HMOs, registering with the university's accommodation service is essential

- Referrals from existing tenants — Often the highest-quality leads

Room Pricing Strategy

Pricing individual rooms requires more nuance than pricing a whole property. Consider:

- The size and specification of each room (en-suite rooms command a premium)

- Local comparable room rents (check SpareRoom and Rightmove)

- Whether bills are included (inclusive pricing simplifies marketing and can justify higher headline rents)

- The quality of communal areas (a refurbished shared kitchen and living room adds value to every room)

All-Inclusive vs Bills Separate

Many HMO landlords offer all-inclusive rents covering utilities, broadband and council tax. This simplifies the tenant experience and reduces disputes. The downside is the risk of high utility usage eating into your margins.

Others charge a lower base rent with bills split between tenants or charged separately. This shifts consumption risk to tenants but adds administrative complexity.

The right approach depends on your target market and local norms.

Tenant Referencing for HMOs

Thorough referencing is just as important for HMO tenants as for whole-property tenants. A standard reference should include:

- Identity verification

- Right to rent check (mandatory under the Immigration Act 2014)

- Employment/income verification

- Previous landlord reference

- Credit check

The cost of a bad tenant in an HMO is amplified because they share space with your other tenants. One problematic tenant can cause several others to leave.

Reducing Void Periods

The keys to minimising voids in an HMO:

- Price competitively — an empty room at £500/month generates less than an occupied room at £475/month

- Maintain the property well — tenants (and their referrals) come from well-maintained, clean properties

- Start marketing before the current tenant leaves — aim for a 2–3 week overlap

- Offer flexible move-in dates — this can capture tenants who need accommodation immediately

- Build community — tenants who enjoy living in the house stay longer and recommend it to friends

Best Cities for HMO Property in 2026

Location is everything in HMO investment. The best HMO locations combine strong rental demand, affordable purchase prices, a growing population of young professionals or students, and reasonable regulatory conditions.

What Makes a Good HMO Location?

Look for:

- Strong rental demand: University towns, cities with major employers, areas with good transport links to employment hubs

- Affordable entry prices: The economics of HMO conversion work best where purchase prices are moderate relative to achievable room rents

- Growing population: Net inward migration, growing student numbers, expanding employment opportunities

- Reasonable regulation: While licensing is unavoidable, some councils are more HMO-friendly than others

- Low existing HMO saturation: Too many HMOs in one area can suppress rents and trigger tighter planning restrictions

Top UK Cities for HMO Investment

Below is a snapshot of popular cities for HMO investment. For financing options specific to each location, follow the links:

- Manchester — Strong young professional market, major regeneration, growing population. Manchester HMO mortgages →

- Birmingham — The UK's second city, major infrastructure investment (HS2 Curzon Street), expanding universities. Birmingham HMO mortgages →

- Liverpool — Some of the highest HMO yields in the UK due to low purchase prices and strong student demand. Liverpool HMO mortgages →

- Leeds — Major university city with a large young professional market and growing financial services sector. Leeds HMO mortgages →

- Bristol — High demand, affluent tenant base, but higher entry prices. Bristol HMO mortgages →

- Nottingham — Two major universities, affordable purchase prices, strong yields

- Sheffield — Growing student population, large-scale city centre regeneration

- London — Huge demand and highest room rents, but extremely high entry prices and complex regulation. London HMO mortgages →

- Coventry — Fast-growing student city, affordable prices, good yields

- Leicester — Growing population, two universities, excellent transport links

Looking for location-specific financing? Get a quote for HMO mortgages in your city →

The HMO Conversion Process (Step by Step)

Converting a standard residential property into a compliant, profitable HMO involves seven key stages. Here's the full process.

Step 1 — Finding a Suitable Property

Not every property makes a good HMO. Look for:

- Minimum 4 bedrooms (ideally 5–6 for better economies of scale)

- Adequate communal space for a shared kitchen and, ideally, a living area

- Layout that works — rooms should ideally be accessible from a communal hallway rather than through other rooms

- Proximity to demand — near a university, hospital, business park or transport hub

- Not in an over-saturated HMO area — check local HMO concentrations and any Article 4 restrictions

Step 2 — Planning Permission & Article 4 Check

Before exchanging contracts:

- Check whether the area is covered by an Article 4 direction

- Confirm the current planning use class (C3, C4, or Sui Generis)

- If planning permission is required, submit an application and wait for approval before committing — or factor the risk into your offer price

Step 3 — Securing Finance

Arrange your financing before works begin:

- If the property is habitable and already suitable for HMO use, apply for an HMO mortgage directly

- If conversion works are needed, arrange bridging finance to fund the purchase and refurbishment

- Get a Decision in Principle (DIP) early so you can move quickly when you find the right property

- Use our HMO mortgage calculator to model your costs and returns

Step 4 — Refurbishment & Building Regs

Typical HMO conversion works include:

- Adding bedrooms (subdividing larger rooms, converting reception rooms or lofts)

- Installing en-suite shower rooms where space allows

- Upgrading the kitchen to accommodate the number of occupants

- Fire safety works (FD30 doors, alarm system, emergency lighting, fire extinguishers)

- Electrical upgrades and rewiring as needed

- Damp-proofing, insulation and general decoration

All works must comply with Building Regulations. Structural changes, new bathrooms and electrical work will require sign-off.

Step 5 — Licensing Application

Apply for your HMO licence as soon as the property is ready for occupation (or before, if your council allows pre-applications). Have all required documents ready:

- Floor plans with room dimensions

- Gas safety certificate

- EICR

- Fire risk assessment

- EPC

Step 6 — Furnishing & Setup

HMO rooms are almost always let furnished. Budget for:

- Double bed and mattress

- Wardrobe and chest of drawers

- Desk and chair

- Bedside table and lamp

- Curtains or blinds

- Communal area furnishings (sofa, dining table, kitchen appliances)

- Broadband installation

Total furnishing cost typically ranges from £1,000–£2,000 per room for a mid-range specification.

Step 7 — Marketing & First Tenants

With the property compliant, furnished and licensed, it is time to fill the rooms:

- Create high-quality listings with professional photographs on SpareRoom, OpenRent and other platforms

- Set competitive rents based on local comparable rooms

- Schedule viewings efficiently (group viewings save time)

- Complete thorough tenant referencing

- Issue compliant tenancy agreements (ASTs with HMO-specific clauses)

- Provide the house handbook, gas and electrical certificates, EPC, and How to Rent guide

Ready to begin? Compare HMO mortgage rates →

HMO Property Glossary

Understanding the language of HMO property is half the battle. We maintain a comprehensive HMO glossary with over 100 defined terms covering everything from Article 4 directions to yield calculations.

Here are 20 of the most commonly searched HMO terms:

| Term | Definition |

|---|---|

| HMO | House in Multiple Occupation — a property let to 3+ tenants from 2+ households |

| Article 4 Direction | A planning order removing permitted development rights for C3 to C4 conversion |

| C4 Use Class | Planning classification for small HMOs (3–6 occupants) |

| Sui Generis | Planning classification for large HMOs (7+ occupants) and other unique uses |

| Mandatory Licensing | Required for HMOs with 5+ tenants from 2+ households (all councils) |

| Additional Licensing | Discretionary council scheme extending licensing to smaller HMOs |

| Selective Licensing | Discretionary scheme requiring all rented properties in an area to be licensed |

| FD30 Fire Door | A fire door rated to resist fire for 30 minutes |

| EICR | Electrical Installation Condition Report — required every 5 years |

| Gas Safety Certificate | Annual inspection certificate for gas appliances by a Gas Safe engineer |

| HHSRS | Housing Health and Safety Rating System — council risk assessment methodology |

| Section 24 | Tax rule restricting mortgage interest deduction for individual landlords |

| SPV | Special Purpose Vehicle — a limited company set up to hold property |

| LTV | Loan-to-Value — the mortgage amount as a percentage of the property value |

| Bridging Finance | Short-term loan used to purchase/refurbish before long-term refinancing |

| Rent Repayment Order | Tribunal order requiring a landlord to repay up to 12 months' rent |

| EPC | Energy Performance Certificate — minimum rating E required for letting |

| Awaab's Law | Legislation setting timescales for landlord response to damp and mould |

| Fire Risk Assessment | Legal requirement to identify and mitigate fire hazards in an HMO |

| Permitted Development | Planning rights allowing certain changes of use without a formal application |

For full definitions and related articles, visit our HMO glossary →

Frequently Asked Questions

How many tenants make a property an HMO?

A property becomes an HMO when it is occupied by three or more tenants who form two or more separate households and share facilities such as a kitchen or bathroom. This definition comes from the Housing Act 2004. Mandatory HMO licensing applies at a higher threshold: five or more tenants from two or more households.

Do I need planning permission for an HMO?

It depends on the size and location. Small HMOs (up to 6 occupants, C4 use class) are normally permitted development and do not require planning permission — unless an Article 4 direction applies in your area. Large HMOs (7+ occupants, Sui Generis) always require planning permission. Check with your local planning authority before proceeding.

How much does an HMO licence cost?

HMO licence fees vary by council. Most charge between £500 and £1,500 for a five-year mandatory licence. Some London boroughs and larger cities charge up to £1,800. Fees are typically payable in two parts. Check your local council's website for exact fees.

What is the minimum room size for an HMO?

The national minimums set by the 2018 regulations are: 6.51 m² for a single room (one person aged 10+), 10.22 m² for a double room (two persons aged 10+), and 4.64 m² for a child under 10. Rooms below 4.64 m² cannot be used as sleeping accommodation. Your local council may impose higher minimums through licence conditions.

Can I get a mortgage on an HMO property?

Yes, but you need a specialist HMO mortgage — standard buy-to-let mortgages are not suitable. HMO mortgages typically require a 20–25% deposit and the borrower to have prior landlord experience. Rates are slightly higher than standard BTL. You can compare HMO mortgage rates on our site.

Is HMO property a good investment in 2026?

HMOs continue to offer higher yields (typically 8–15%) than standard buy-to-let (4–7%), with reduced void risk due to multiple income streams. Strong demand from young professionals and the ongoing affordability crisis support the market. However, HMOs require more management, more upfront capital, and navigating a complex regulatory environment. They suit active, hands-on investors who are prepared for the additional workload.

What insurance do I need for an HMO?

You need specialist HMO landlord insurance that covers buildings, contents (landlord furnishings), public liability and legal expenses. Standard buy-to-let insurance will not cover an HMO and could void your policy entirely. Rent guarantee insurance is optional but recommended. Read our HMO property insurance guide for full details.

What is an Article 4 direction?

An Article 4 direction is a planning order made by a local authority that removes permitted development rights in a specified area. In the context of HMOs, it means you need full planning permission to convert a dwelling house (C3) to a small HMO (C4), even though this would normally be allowed automatically. Article 4 directions are common in university cities and areas with high HMO concentrations.

How are HMO properties valued?

Smaller HMOs are usually valued on a bricks and mortar basis — comparable to similar residential properties in the area. Larger HMOs (7+ rooms) may be valued on a commercial basis using a capitalisation rate applied to rental income. The valuation method affects how much you can borrow when remortgaging. See our guide on how HMO properties are valued.

What is the difference between C4 and Sui Generis?

C4 is the planning use class for small HMOs housing 3–6 unrelated occupants. Sui Generis (Latin for "of its own kind") covers large HMOs with 7 or more occupants and falls outside the standard use class system. The key practical difference is that converting to Sui Generis always requires planning permission, while C4 is often permitted development (unless Article 4 applies).

This guide is updated regularly to reflect the latest legislation and market conditions. Last updated: March 2026.

The HMO Mortgage Broker is a specialist HMO mortgage comparison and resource site. We do not provide financial advice. Always seek independent professional advice before making financial decisions.